A downturn has plagued the mass media markets since 2012. The coming few years will show whether publishing – and the media field more broadly – will be able to renew in the midst of the transition and rise from financial difficulties.

The mass media market volume grew steadily in the second half of the 1990s but the growth slowed down at the start of the millennium. Before the financial crisis started, the annual growth on the media markets amounted to three to four per cent. Since 2012, the media markets have contracted every year. Also relative to GDP (mass media markets/GDP, %), the value of the mass media has decreased.

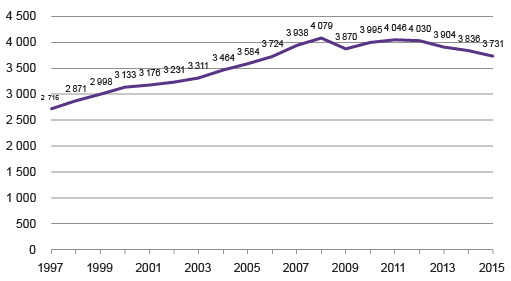

The value of the Finnish mass media market was about EUR 3.7 billion in 2015 (Figure 1). The market volume decreased by around three per cent from the year before.

Figure 1. Mass media markets in 1997 to 2015, EUR million

Source: Statistics Finland, mass media and cultural statistics

The media market can be divided into three:

- Publishing that includes the press and publishing of books;

- Electronic media that includes national, regional or local radio and television activities, as well as the new media or media services on the Internet;

- Recorded media that includes all sound and video recordings, cinema ticket sales and cinema advertising.

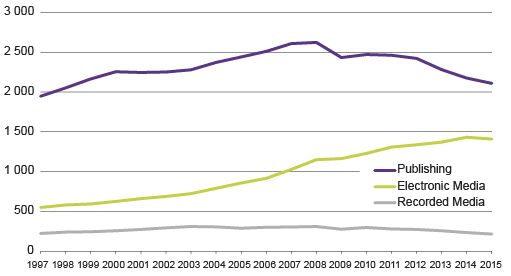

In the current decade, the share of publishing in the media markets has decreased dramatically and the share of electronic media has grown. So a transition is ongoing in the market structure. How is the transition visible in the various media market sectors and why has the transition not generated growth?

Hard times for publishing

In 2015, the share of publishing (papers, books) in the media markets was 57 per cent. Thus, publishing is still the largest sector of the media markets in Finland. Its value and share have, however, declined clearly when comparing with 2000 when the share of publishing was as high as 75 per cent of the mass media markets (Figure 2).

Figure 2. Mass media markets by sector in 1997 to 2015, EUR million

Source: Statistics Finland, mass media and cultural statistics

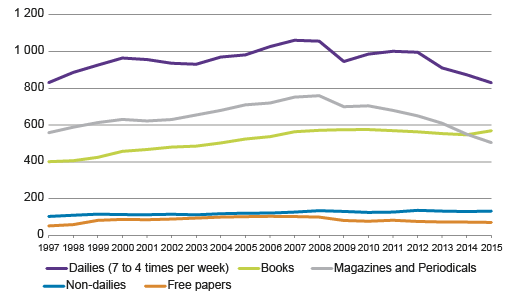

In 2015, net sales of dailies, non-dailies and free papers totalled around EUR one billion (Figure 3). Newspapers (dailies, papers published three to one times per week and free papers) are an important segment in the mass media market measured by the economic value and with around 28 per cent market share. However, the share of newspapers has decreased as a result of changes in the income formation and circulation development.

Figure 3. Publishing in 1997 to 2015, EUR million

Source: Statistics Finland, mass media and cultural statistics

At the end of the 1980s, dailies received even over 70 per cent of their revenue from ad sales (all classified ads included), and even in 2000 the share was close on 60 per cent. In 2015, the share of ads was only around 45 per cent of the income of dailies.

In addition to advertising, newspapers have received their revenue from a variety of circulation income (subscriptions and single-copy sales). The total circulation of dailies was around 1.6 million in 2014. Between 2004 and 2014, the circulation of all major dailies, and especially afternoon papers, has fallen. The circulation of afternoon papers has dropped by 45 per cent in ten years.

The number of readers of printed papers have also plummeted. Readers have largely migrated to using the web services of newspapers. Both Iltalehti and Ilta-Sanomat are at the top of the list of the most popular online media services.

The digital revolution is both fast and slow. The share of digital income in 2015 corresponds with nine per cent of the total sales of all newspapers. This is naturally not nearly enough to cover the income losses of printed papers.

The drop in circulation is largely explained by consumers – and advertisers – moving to electronic mass media but also by the abundant supply of free media content, which has lowered consumers’ willingness to pay for mass media companies’ services.

Free media content is available, e.g. through Facebook and other social media services, city papers, radio, international online media, blogs and online publications. In addition, the Finnish Broadcasting Company, MTV and national newspapers offer free media content on their websites.

Researchers from VTT Technical Research Centre of Finland and the University of Turku have described the disruption (the breakdown of established practices) caused by digitalisation in publishing. They place the disruptive turn in publishing at 2012. Due to weakened preconditions for activity, companies have been forced to change their operational strategy. A crisis threatens the existence of publishers and they must respond. (Södergård et al. 2016.)

Companies in the media field have reacted to the challenges by, e.g. developing digital services, cutting costs, increasing operational efficiency and strengthening their competitive position on the media markets (Kleis Nielsen et al. 2016). Conventional mass media companies have been active in developing so-called integrated communication products and services as early as the 1990s. Finland’s most popular media-focused web pages are even now mostly maintained by conventional mass media companies.

The measures have generated some results. For example, Helsingin Sanomat has managed to increase the share of readers who, in addition to the printed paper, also pay for the digital version of the newspaper. (Södergård et al. 2016.)

The coming years will show whether these efforts will bear fruit. Will publishing – and the media more broadly – be able to renew in the midst of the transition and rise from the financial difficulties? At the moment, the industry seems to be waiting for help from the end of the economic downturn and a general pickup in the economy.

Huge growth in electronic media

Over the past ten years, online media has grown rapidly (by 320% in 2005 to 2015), but the growth in television activities (43%) can also be seen as an important change. The share of electronic mass media on the mass media markets has nearly doubled since 2000. In total, the value of the electronic mass media market at end user level was EUR 1.4 billion in 2015. (Figure 4.)

Figure 4. Electronic media in 1997 to 2015, EUR million

Source: Statistics Finland, mass media and cultural statistics

Currently, television activities form around 75 per cent of the electronic communication market.

The turn of the millennium was a time of slow growth for television. Advertising revenue for television, like print advertising, actually declined during a couple of years. The television sector started growing rapidly in the later years of the digitalisation process (2007 to 2008) when the growth conditions for, e.g. pay TV markets matured.

The biggest income item of television activities in Finland is the public service broadcasting tax with a share of over 40 per cent. The share of advertising has decreased to one-quarter of the income of television activities. The share of pay TV in the income of television activities has grown since 2007 and is now around one-third of the activities. Video streaming services (e.g. Netflix, HBO, Viaplay) are included in the pay TV subscription figures in the media market calculations.

The income of commercial radio activities are nearly purely advertising revenue. The income of commercial radios grew quickly in the early 2000s but then the growth halted for years to around EUR 50 million. The financial crisis did not have much effect on commercial radio activities, and in the past few years the income for radio activities has been around EUR 60 million. The share of commercial radio in total media advertising is around five per cent.

The share of Internet advertising on the mass media markets has grown during this century from zero to around eight per cent in 2015. The figure includes web media advertising, electronic directories and search engine advertising.

Around EUR 286 million was spent on Internet advertising, which is one-quarter of total media advertising. Over the past few years, the volume of web advertising has exceeded that of TV advertising. In the other Nordic countries, web media advertising surpassed TV advertising clearly earlier than in Finland.

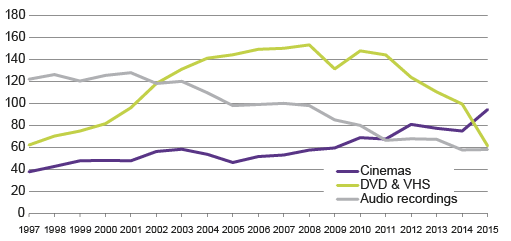

Recorded media sales have plummeted

The share of recorded media (including sound and video recordings, cinemas) on the media markets was growing in the early 2000s but especially in the 2010s, the share of this market segment has declined clearly below the level at the turn of the millennium. The sales of sound recordings dried up first and then also those of video recordings.

In 2015, recorded media sales totalled good EUR 200 million and their share of the mass media markets was around six per cent. On the other hand, 2015 was especially lucrative for cinema sales (incl. ticket sales and cinema advertising): EUR 94 million or 26 per cent more than in the year before. (Figure 5.)

Figure 5. Recorded media in 1997 to 2015, EUR million

Source: Statistics Finland, mass media and cultural statistics

The volume of sound recording sales has been decreasing since the beginning of the 2000s and in 2003, the sales volume of video recordings surpassed that of sound recordings. The share of digital music sales over the web has grown strongly in the past years. In 2015, the share of digital sales in wholesale trade of sound recordings was 63 per cent, having been 27 per cent in 2012. (Statistics by IFPI Finland).

The rapid growth in digital sales has not, however, prevented the total market for recordings from subtracting. From 2005 to 2015, the value of Finland’s recorded media sales (physical recordings and online sales) have decreased by 40 per cent.

The sales of video recordings grew still in the first decade of the 2000s but in the past few years, sales have made a steep downturn. In 2015, video recordings were sold and rented for a total of around EUR 60 million.

The audiences and income of cinemas made an upturn after the mid-1990s when the popularity of domestic films started growing. However, cinemas account for only two per cent of the total media markets.

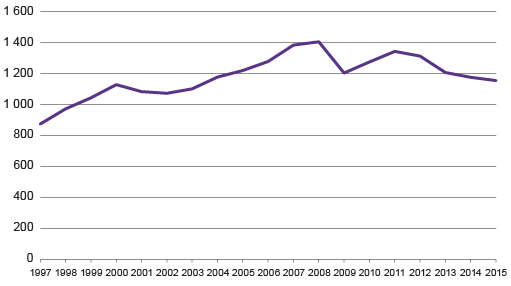

Media's advertising pot has been depleting since 2012

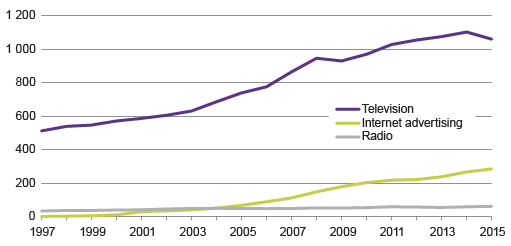

Media advertising is a crucial part of media market activities. In 2015, EUR 1.2 billion was spent on media advertising in Finland. During this millennium, the amount of euros spent on media advertising has varied between EUR 1.1 and 1.4 billion. (Figure 6.)

Figure 6. Media advertising in 1997 to 2015, EUR million

Sources: The Finnish Advertising Council, Kantar TNS (former TNS Gallup Oy)

As a result of the transition caused by the digitalisation process, competition for both advertisers and paying customers has tightened. Digitalisation has challenged, in particular, the old business model of newspapers and magazines when a majority of the ad money that used to act as the cornerstone of the press has followed consumers to electronic media. Media's advertising pot has also been depleting since 2012.

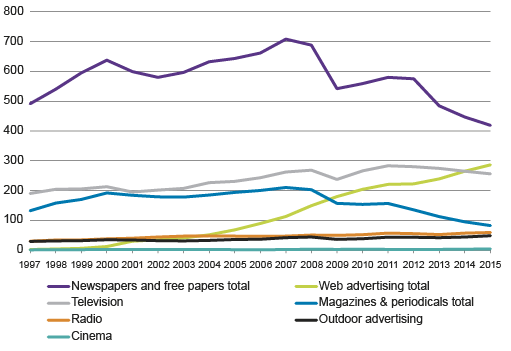

Despite this, Finland is still a fairly newspaper-focused country when it comes to media advertising, even though the share of newspaper advertising in media advertising has decreased clearly over the past ten years (Figure 7).

Figure 7. Media advertising by type of media in 1997 to 2015, EUR million

Sources: The Finnish Advertising Council, Kantar TNS (former TNS Gallup Oy)

The share of newspaper advertising in all media advertising has seen a trend-like decline. It was, including free papers, clearly over fifty per cent still in the early 2000s but only 36 per cent in 2015. In 2007, the value of media advertising in newspapers (incl. city papers) was EUR 708 million and in 2015 only EUR 419 million.

The development trend of magazine advertising in Finland was on the rise for a long time, i.e. contrary to many other European countries. As a result of the financial crisis, in 2009 alone, nearly one-quarter of magazine advertising disappeared. In 2015, the share of magazine advertising had decreased to around seven per cent.

What has slowed down digital sales?

Following newspapers and magazines in digital format has become more common in the 2010s: a considerable share of readers have stopped reading printed papers. A paper printed in the spring of 2011 reached, according to Kansallinen Mediatutkimus (the National media survey) 94 per cent of respondents but in the autumn of 2016 only 75 per cent of respondents had read a printed newspaper at least once a week.

Simultaneously, 48 per cent said they read newspapers on a computer, 45 per cent on a mobile phone and 28 per cent on a tablet or eReader at least once a week. Following newspapers through a computer screen has decreased in recent years but reading via a tablet, eReader and especially a mobile phone has become more common.

In 2015, digital income still formed a relatively small share of newspaper income (around nine per cent in Finland, six per cent in World Press Trends’ international comparison) (WPT 2016). What has slowed down the growth in the share of digital sales?

The advertising income collected online by publishers has not been nearly enough to cover the income loss from printed advertising as online advertising is cheaper than conventional advertising channels. The revenue models are still the main challenge for the development of media enterprises’ online publications.

The value of advertising in online media was roughly EUR 286 billion in 2015. The press’ share of online advertising income is considerable (around one-fifth), but compared to the income flow from printed paper advertising the volume is still modest.

The press seeks to find efficient models to make income based on their online content in a way that would compensate for the drop in printed media circulation and advertising income. Chargeable services and paywalls have become more common and newspaper enterprises have thus tried to wean users from the assumption of free services.

There are three types of paywalls: the freemium model, the metered model and the so-called hard wall. In the freemium model, part of the content is free and part is chargeable. In the metered model, the user can view a specific number of articles over a limited time. In the hard paywall model, all content is chargeable and the reader can at most access only captions for free. Some papers combine different types of paywalls in a so-called hybrid model.

Despite increased popularity of paywalls, there is still a lot of free content available. According to Suomen Lehdistö’s (Finland’s press) report, ten of 27 dailies did not have any chargeable content on their website in 2016. Two papers had given up their once launched paywalls. (Suomen Lehdistö, 3/2016.)

Paywalls can also be bypassed. A very extensive news flow from several sources can be followed through Facebook free of charge. Facebook has increasingly become more of a media company type of operator, which is now also recognised by the company’s management. Even though the company does not produce its own news articles, it exercises editorial power when it values different media content. (E.g. Mainonta & Markkinointi.)

In 2015, Facebook launched instant articles, where an article published by a media company is located on Facebook’s server and can be read from there for free. This publication type serves the reader, for example, in that the article loads more quickly but people have also seen risks for the publishers in this arrangement. Facebook offers some of the advertising money to the publishers of instant articles but there are contradictory views on the financial benefits of this form of publishing for the publishers.

In Finland, newspaper content shared through social media has not thus far replaced the following of newspaper content through the websites of the newspapers.

The third reason for the slow growth in the share of digital sales is the effect value added tax has on the pricing of digital content. Digital publishing has been taxed more heavily (24%) than printed content (10%). The arrangement has been based on European regulations.

In 2016, the European Commission finally decided to propose that the VAT treatment of printed and digital papers and books should be harmonised. A decision on the new VAT treatment still requires approval from all member states. After that, the level for digital VAT is decided by local decision-makers. It is appropriate to assume that as a result of the tax decision, the consumer prices for digital papers and ebooks will decrease.

Government now subsidises the press with only EUR half a million per year. Subsidies are granted to “papers published in national minority languages and corresponding online publications”. The lowered VAT rate for subscribed newspapers and magazines can, however, be considered as indirect financial press support.

A change took place in the subsidy measures in the 2010s when the zero tax rate that had been in use was removed at the end of 2011. (Sales used to be tax free, the VAT included in input purchases was returned to the seller). The adoption of VAT had a disruptive effect: the subscription prices of papers rose, while consumers started to find (free) digital and mobile media content. (Södergård et al. 2016.)

The fourth reason for the slow growth in newspapers’ digital sales is connected to the population structure and the consumption cultures and opportunities of different population groups: While nine in ten persons aged under 45 read online papers or TV channels’ news sites, under one-half of pensioners do so (Use of information and communications technology by individuals).

Especially young people consume digital media content. Next to the very elderly, young people are the population group where being at-risk-of-poverty is more common than the average for the whole population (Income distribution statistics). A weak financial situation is bound to affect young people’s liquidity both in terms of digital and printed media content.

Naturally, young people are not the only population group with meagre resources. Following of online content is also divided by level of education so that highly educated people follow media content on the web clearly more than less educated people. (Use of information and communications technology by individuals).

Paying for online content is a habit one can learn

The development of the mass media market has been eventful over the past two decades. The transition has primarily been caused by the digitalisation of the media economy, which is linked to increased advertising in electronic media and decreased advertising in printed media. The media markets have contracted over several years starting from 2012; by around three per cent from 2014 to 2015.

The 2010s have been a period of major change especially for newspapers. In order to survive, publishers have been forced to renew their business model, cut costs and create new forms of cooperation. They wish to announce the era of free content as the past and many dailies have introduced different types of paywalls on their websites.

On the other hand, there has been indications of free media content possibly not being the most attractive alternative for consumers after all. According to a report from the Reuters Institute in October 2016, paying for online content is a habit one can learn and that is becoming more common. According to the report from the Reuters Institute, young people are more likely to pay for media content if they are used to paying for, e.g. Netflix (video on demand) or Spotify (music). (Reuters Institute Digital News Report 2016.)

The latest challenge for newspapers’ business model comes from social media (especially Facebook). Presence on social media offers newspapers visibility and the possibility to market their product but social media offers consumers the chance to bypass paywalls and follow news flow that simultaneously covers several news sources for free. The relationship of the press with technology giants is an interesting factor to follow in future.

It is evident that consumers who bypass paywalls are interested in media content. In this sense, the mass media is doing well. Interest in media content has not decreased and according to the TNS Atlas survey, Finns spend an average of eight hour per day following the mass media. What type of service consumers are prepared to pay for and at what price is a tricky question. It is highly likely that interesting times will continue in the media industry.

--------------------------------------------------------------------------

Mass media statistics

Industry-specific data concerning total mass media markets are based on several data sources. The data concerning several industries are rough estimates. Turnover calculations have been made at the culture and time use unit of the Population and Social Statistics Department at Statistics Finland in cooperation with external experts.

The calculations describe the end user level: for example, the figure on the newspaper market is comprised of retail priced subscription and single copy sales of newspapers, and their revenue from advertising.

Possible overlaps in the figures have been eliminated when possible and ,thus, the figures for the different industries are mutually exclusive.

The figures cover domestic production and imports but not enterprises’ foreign activities.

To be exact, this is not the established concept for enterprises’ turnover used in economics but it is, however, often used when discussing the financial volume of the mass media.

Statistics on mass media have been compiled into a table package on Statistics Finland’s website.

---------------------------------------------------------------------------

Kaisa Saarenmaa is Special Editor responsible for statistics on mass media at the Population and Social Statistics Department at Statistics Finland. Tuomo Sauri is a retired Senior Researcher from the same department.

References:

IFPI Finland ry. Statistics.

Kleis Nielsen, Rasmus & Cornia, Alessio & Kalogeropoulos, Antonis (2016). Challenges and opportunities for news media and journalism in an increasingly digital, mobile, and social media environment. Reuters Institute for the Study of Journalism.

Mainonta & Markkinointi 2.1.2017. Myöntääkö Zuckerberg vihdoinkin, että Facebook on mediayhtiö?

Reuters Institute Digital News Report 2016.

Suomen Lehdistö 3/2016. Valintojen maailma.

Södergård, Caj & Bäck, Asta & Koiranen, Ilkka (2016). Kustantaminen esimerkkinä digitalisaation aiheuttamasta toimialan disruptiosta. Talous & Yhteiskunta 3/2016.

Statistics Finland. Mass media statistics table service.

Statistics Finland. Income distribution statistics.

Statistics Finland. Use of information and communications technology by individuals.

TNS Atlas Intermedia 2015.

World Press Trends 2016: Facts and Figures.